![]()

The Financial Intelligence Unit has its daggers drawn against EcoCash. The unit’s Acting Director General wants his pound of flesh and he’s not taking any prisoners.

Background

Zimbabwe’s currency is tanking on the only market that matters in this country: the parallel market. This is not coming as a surprise to anyone except maybe the people whose policies have brought us here- those fellas prefer to live in denial. From their lofty place in denial, the powers that be namely the Reserve Bank of Zimbabwe and the FIU have decided that their scapegoat is EcoCash.

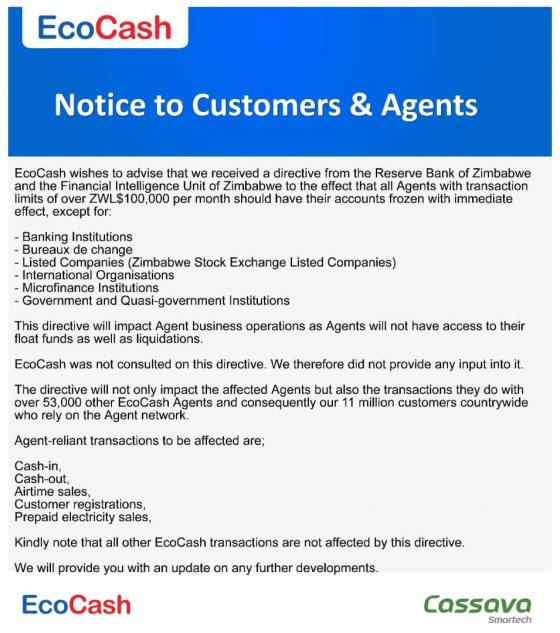

Just over two weeks ago, the FIU issued a directive for EcoCash to freeze the accounts of all agents that transacted above ZW$100,000 per month. This was USD4,000 at the time. Instead of complying, EcoCash rushed to court filing an urgent application to have this directive suspended.

In the intervening time, the RBZ issued new notes into the economy. As soon as they did that the local currency tanked further by 40%. Of course, in the eyes of the RBZ this is EcoCash’s fault. If only the authorities could see or at least entertain the thought that Zimbabweans don’t trust them. When they issue bank notes, the natural thing for the citizens to do is to reject such notes in favour of the USD. As with most economic phenomena, the doom prophecy by the public is self fulfilling: the currency crashes. But no, according to the RBZ, EcoCash is the responsible demon.

This brings us to now. The FIU wrote to Steward Bank, EcoCash’s sister company which is the mobile wallet’s sponsor bank for settlements. The letter instructed Steward Bank to limit agent to agent transactions on the EcoCash trust account among other things.

In another letter to EcoCash CEO, Natalie Jabangwe dated 19 May 2020, the FIU Acting Director General notified Jabangwe and her boss, Cassava CEO, Eddie Chibi of intention to impose administrative penalties on the two executives as well as on EcoCash itself. What are the charges and what do they mean? Is there a case to answer by EcoCash and its executives? Let’s explore that:

The charges

1. Failure to comply with any mandatory requirement of a circular, directive or guideline issued in terms of the Act (Item 26 of Table of Civil Infringements. AML/CFT Directive No. 2 of 2014)

When EcoCash was directed to freeze the accounts of agents who transacted above ZW$100,000 per month, the EcoCash management didn’t comply. Eddie Chibi instead approached the High Court seeking immediate reprieve and suspension of the directive.

In his founding affidavit, Chibi argues that the directive issued by the FIU was illegal. His key reason to conclude that is that EcoCash and its agents had not been heard. He wrote:

The Applicant and its Agents have a right in terms of the law to lawful and rational administrative action by the Respondent. This means that the Applicant and the Agents had a right in terms of the common law and in terms of the Administration of Justice Act Chapter 10:28 to be heard before a decision is taken that affects their rights in the Ecocash system. The right to be heard is a fundamental right in our law that is also protected by the Constitution of Zimbabwe, the supreme law of the land.

The respondent referred to is the RBZ

Chibi goes on to say that the directive issued by FIU was irrational in that it does not specify the crimes committed by the agents and would make it seem as if merely transacting above $100,000 per month was a crime. Repeatedly Chibi goes back to the issue of not having exercised his right to be heard and this seems to be the chief argument. He also says the ACT under which the directive was issued did not give the FIU power to make such a directive:

I contend that the provisions of section 10 only authorise the Respondent to act if the management of the system itself has done or omitted to do something. The Applicant is not punishable where some users of the system are alleged to have themselves committed an abuse. The approach, in that case, is to penalise defaulting users. In the present matter, no allegation of illegality has been made or proved against the Agents and in the absence of that, there is no basis for the Respondent to seek reliance on section 10.

He goes on:

Thirdly, the powers of the Respondent in terms of section 10(1)(i)-(iii) are limited. The Respondent can issue a directive directed against specific conduct, a directive for something to be done to remedy a situation or to provide the Respondent with certain information. The provisions of section 10(1)(i)-(iii) do not give the Respondent power to suspend an Agent from participating in the Ecocash system. in the event of a troublesome Agent, the directives that the Respondent can issue can be enforced in terms of sections 10(2)-(4) of the Act.

Whether or not Chibi is right doesn’t matter. The directive was issued and the directive should have been complied with whether or not EcoCash believed it to be legally flawed. EcoCash was well within its rights in going to court, they should have done so while still complying until the court decided to grant them the reprieve or ultimately the decision they sought.

It looks as if EcoCash gambled that their urgent application would sail through. The reality is that it didn’t and so, the first charge against them stands: they did not comply with a directive issued under an ACT of parliament.

It also doesn’t matter that FIU’s original directive was ridiculous. In January last year, Econet (EcoCash’s former parent and current associate) complied with an illegal and ridiculous directive to shut down the internet. Their argument was that they could not ignore it until a court decided on the legality or lack of it.

2. Failure to comply with any obligation relating to customer identification and /or verification (Item 2 of Table of Civil Infringements, AML/CFT Directive No. 2 of 2014)

The FIU leveled this one with alternatives:

Alternative A: Failure to maintain books and records as required under section 24 of the Act (Item 2 of Table of Civil Infringements, AML/CFT Directive No. 2 of 2014)

Alternative B: Failure to timely avail to the FIU, upon request, books and records referred to in section 24 of the Act or any information contained therein (Item 14 of Table of Civil Infringements, AML/CFT Directive No. 2 of 2014)

This one sticks. The FIU alleges that when they directed EcoCash to freeze accounts of agents that transacted above ZW$100,000 per month they also directed EcoCash to furnish them with KYC details for some 96 agents they suspected of illicit activities. According to the FIU, EcoCash stalled and did not meet the 2 day deadline to submit this information.

The FIU says EcoCash submitted incomplete information two weeks later. Chiperesa wrote:

Even after taking two weeks to run around and put together some information, Ecocash still could not provide names of a CEO/MD even of one agent, nor the list of directors, list of shareholders and ultimate beneficial owners as requested by the FIU and as required by law. Although Ecocash, in the end, provided purported business addresses for some of the agents, in most cases the addresses were incomplete or patently false/fictitious.

All this led Chiperesa and his unit to conclude that EcoCash did not have the relevant KYC documents which they should have had by law. This is in the realm of possibility when you consider the history of EcoCash’s founding. It started off as mostly a peer to peer remittances solution. Users would ‘cash-in’ just so they could send money to friends and relatives who would then ‘cash-out’ soon after receipt.

To make all this possible, EcoCash went on a massive drive to recruit agents who would facilitate the ‘cashing in and out’ in exchange for a commission. Most of the agents were small traders who already operated community businesses allowing them to have the necessary float to facilitate the transactions. Our speculation is that there wasn’t a rigorous KYC requirement to become such an agent and there probably wasn’t much need for such. These were micro transactions performed by a network of small businesses (Most of them informal).

EcoCash evolved though. It became first a wallet were users would actually keep their money- a bank account if you will. It wasn’t merely an instrument for sending and receiving money anymore. Beyond that, EcoCash became a payments platform in fact the most important payment platform as far as retail/consumer payments are concerned. Mobile money accounts for more than 80% of all consumer transactions and EcoCash has above 95% share of the mobile money volumes.

With the increased importance of EcoCash as a platform and the cashless situation Zimbabwe finds itself in, a lot more scrutiny has been placed on the mobile money service. The central bank itself alluded to the fact that EcoCash had become a full fledged financial services company.

It’s highly probable that there are some agents that were recruited over the years that had never submitted full details needed for KYC. Remember, agents are no longer simply intermediaries but they have become EcoCash customers themselves and as customers they must ‘be known’ to EcoCash.

It’s also probable that even recently KYC obligations were not taken as seriously at EcoCash because the culture that stuck during the moving fast days is not so easy to shake off. Added to the mix is the fact that some agents have outgrown the status they had when they first joined the platform.

EcoCash came up with tiers to distinguish agents from other agents and thus apply different KYC standards and transaction limits across. This process is more of a rationalisation and it cannot be simple.

So yes, I have speculated a great deal here but given the history of how EcoCash moved really fast and how things in Zimbabwe changed even faster this speculation is quite probable.

EcoCash probably needs to negotiate with the RBZ for some leeway and a process of rationalising KYC requirements over a more generous timeline. As it is, this charge against them sticks. They are wanting on this.

3. Failure to report a suspicious transaction as required in terms of section 30 of the Act: (Item 21 of Table of Civil Infringements, AML/CFT Directive No. 2 of 2014)

The FIU is alleging that some of EcoCash’s agents were doing high volumes of transactions during the lockdown when economic activity had actually slowed down. Besides the lockdown, FIU says the transactions were already suspicious because they were not tallying with the size and nature of business conducted by the listed agents.

This allegation is odd because Eddie Chibi’s affidavit to the High Court included an attached letter that Natalie Jabangwe had written to the FIU complaining about the FIU’s failure to follow up on suspicious transactions reported by EcoCash.

This one is a bit difficult to make a call on. Crimes of omission are difficult to determine.

4. Disclosing to a customer or to a third party that a suspicious transaction report has been, is being, or will be submitted to the Unit: (Item 24 of Table of Civil Infringements, AML/CFT Directive No. 2 of 2014)

The letter from Natalie Jabangwe to FIU that Eddie Chibi attached in his submission to the High Court has given rise to this charge. Jababngwe’s letter had samples of suspicious transactions that the FIU had not followed up on. The Acting Director General of the FIU says by attaching this letter including the sample transactions, Chibi was in effect notifying entities that had been flagged which he says is illegal. Chiperesa cites the law:

No financial institution or designated non-financial business or profession, nor any director, partner, officer, principal or employee thereof, shall disclose to any of their customers or a third party that a report or any other information concerning suspected money laundering or financing of terrorism will be, is being or has been submitted to the Unit, or that a money laundering or financing of terrorism investigation is being or has been carried out, except in the circumstances set forth in subsection (3) or when otherwise required by law to do so.

He is right of course that Chibi did not need to include these details in his application for an urgent interdict at the High Court. Chiperesa again rightly points out that if Chibi felt that the details were necessary he should have applied to the court to permit such disclosure.

Difficult one for EcoCash

I am no lawyer but all the charges leveled against EcoCash seem to be plausible. They all arise from the fact that when EcoCash received the directive to freeze accounts and submit KYC documents they didn’t comply. The only way out seems to be a ruling by the High Court setting aside the directive before expiry of the 7 day notice period given to EcoCash and its two executives to respond to the charges.

Is EcoCash the cause of our currency problems? Hell no! Zimbabwe’s currency is tanking for no other reason but the fact that our government and central bank are neither trusted nor trustworthy. Zimbabwe’s currency is tanking because several times our bank accounts were raided and real money in there was replaced by fictional money called bond notes or RTGS dollars or ZWL or whatever else will come later. This is where the distrust comes from.

However, the failure by EcoCash to comply with the FIU is a big problem for the mobile payments company. It will be interesting to see how they will come out of this one if they will.

Quick NetOne, Telecel, Africom, And Econet Airtime Recharge

If anything goes wrong, click here to enter your query.

The post Breakdown Of 4 Charges Leveled Against EcoCash, Its CEO And The CEO Of Its Parent appeared first on Techzim.